– Threat of foreclosures: If you can’t help make your home loan repayments just after dollars-aside refinancing, you chance dropping your home so you can property foreclosure. It is vital to determine the money you owe and ensure you can afford the newest home loan repayments prior to going for money-out refinancing.

– Home equity loan: Property equity mortgage is a type of mortgage enabling you to definitely borrow secured on the new collateral in your home. Rather than dollars-aside refinancing, a property collateral financing doesn’t alter your current home loan however, contributes an extra home loan to your house. Family guarantee loans have higher rates than simply dollars-out refinancing, nevertheless they feature straight down settlement costs.

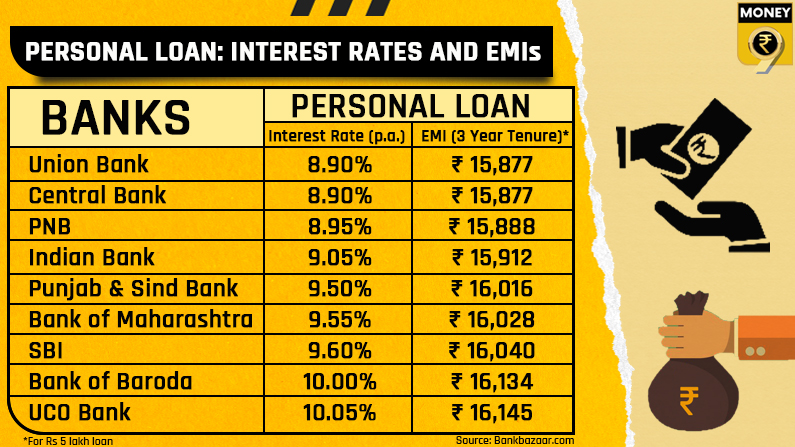

– personal loan: A personal loan are an unsecured loan which you can use for different aim, instance home improvements or debt consolidation. Unsecured loans has highest interest rates than mortgage loans, nevertheless they do not require collateral, and you can have the cash easily.

Your best option to you personally hinges on the money you owe and you may desires. If you have a high-rate of interest on your own newest home loan and require bucks to have a great specific goal, cash-aside refinancing may be a good option. But not, or even have to improve your established home loan or are unable to pay for large monthly premiums, a house guarantee mortgage otherwise consumer loan is a better selection. Its essential to evaluate different choices and you can consult with a financial mentor before deciding.

Cash-aside refinancing should be a strong unit to gain access to the newest security of your house, however it is important to weighing advantages and you can drawbacks prior to going for it. Determine your debts, examine different alternatives, and ensure that one may pay the the home loan repayments before making a decision.

Refinancing can be an attractive option for homeowners who want to reduce their monthly mortgage payment or interest rate. However, it’s important to carefully weighing advantages and disadvantages before making a decision. Refinancing involves replacing your existing mortgage with a new one, which can come with additional charges and you can settlement costs. While it can help you save money in the long run, it’s crucial to evaluate your financial situation and consider all the factors that can affect your long-identity stability.

step 1. down monthly payments: Refinancing can help you lower your month-to-month mortgage repayment for individuals who normally safe a lower life expectancy interest. Such as for example, for individuals who have a thirty-year fixed-speed financial during the 5%, refinancing to help you an effective 4% rate could save you hundreds of dollars a month. This may free up dollars with other expenditures otherwise savings specifications.

Shorten your loan identity: Refinancing may also be helpful you have to pay out of their financial reduced because of the

2. reducing the loan identity. For instance, if you have a 30-year mortgage but refinance to a 15-year term, you could save on interest costs and become debt-free sooner.

step 3. Cash-out refinancing: When you have equity of your property, you are capable of a money-away refinance. This means you acquire more their remaining financial balance and you can get the difference between dollars. This is exactly regularly pay large-desire loans, finance renovations, otherwise safety other expenditures.

step 1. Settlement costs: Refinancing comes with a lot more costs such as for instance settlement costs, assessment charge, and you can name insurance coverage. These could soon add up to several thousand dollars, that can counterbalance the offers out-of a lower rate of interest.

It indicates you’ll end up paying rates of interest once again on the principal, that can extend the life span of the loan while increasing the fresh new full attention can cost you

step three. Certification requirements: Refinancing including is sold with certification standards instance credit score, debt-to-money ratio (DTI), and you may a job records. Or even meet the lender’s standards, you personal loans for bad credit Michigan might not have the ability to re-finance or get a favorable interest.